The advice that outlived its own math

Somewhere in the late 1990s, a financial advisor named David Bach did a piece of arithmetic that would follow us around for the next twenty-five years. Skip a daily latte, invest the difference, and by retirement you would supposedly be sitting on around two million dollars. It was clean, it was quotable, and it quietly pinned the blame for being broke on a paper cup.

There was one problem. The number was never real. A five-dollar-a-day habit works out to $1,825 a year, which Bach rounded up to a friendlier $2,000. He assumed roughly eleven percent annual returns, and he left out both inflation and taxes. When one widely cited finance blog added those back in, the two-million-dollar promise shrank to something closer to a hundred and seventy thousand. Real money — but not the fortune the slogan sold.

The latte was never the villain. It was just the easiest suspect to see.

Why the coffee became the villain

A latte is the perfect thing to feel guilty about. You hand over the card, you watch the number, you can picture the cup in your hand. It is visible, deliberate, and easy to tally. Behavioral economists have a name for the way we file money into little mental drawers — mental accounting — and small, repeated purchases live in the drawer we open most often.

Your rent does not work that way. Neither does your insurance premium, your phone plan, or the streaming bundle that renews while you sleep. Those costs are large, automatic, and boring, so your attention slides right off them. The advice industry pointed at the coffee because the coffee was the one thing you could actually catch yourself buying.

Where the money actually goes

When researchers looked at what really strains a household budget, the coffee barely registered. In The Two-Income Trap, Elizabeth Warren and Amelia Tyagi found that fixed costs — housing, health care, and the price of raising and educating children — had climbed from roughly half of a typical family's income in the 1970s to about three-quarters by the 2000s. The squeeze was not a generation suddenly discovering espresso. It was the big, unavoidable bills eating the breathing room families used to have.

The pattern holds at a smaller scale too. The things most likely to wreck a budget in a single stroke are rarely lattes — they are the rent increase, the surprise medical bill, the car that finally dies, the job that ends. Small discretionary spending can add up over time, but it usually needs one of those larger shocks to actually push someone under.

The trap of chasing small things

Aiming your energy at five-dollar purchases is not just ineffective. It can be actively counterproductive. Willpower is finite, and pouring it into denying yourself coffee one morning at a time is exhausting. People burn out, decide frugality does not work, and abandon the whole project — usually without ever touching the costs that mattered.

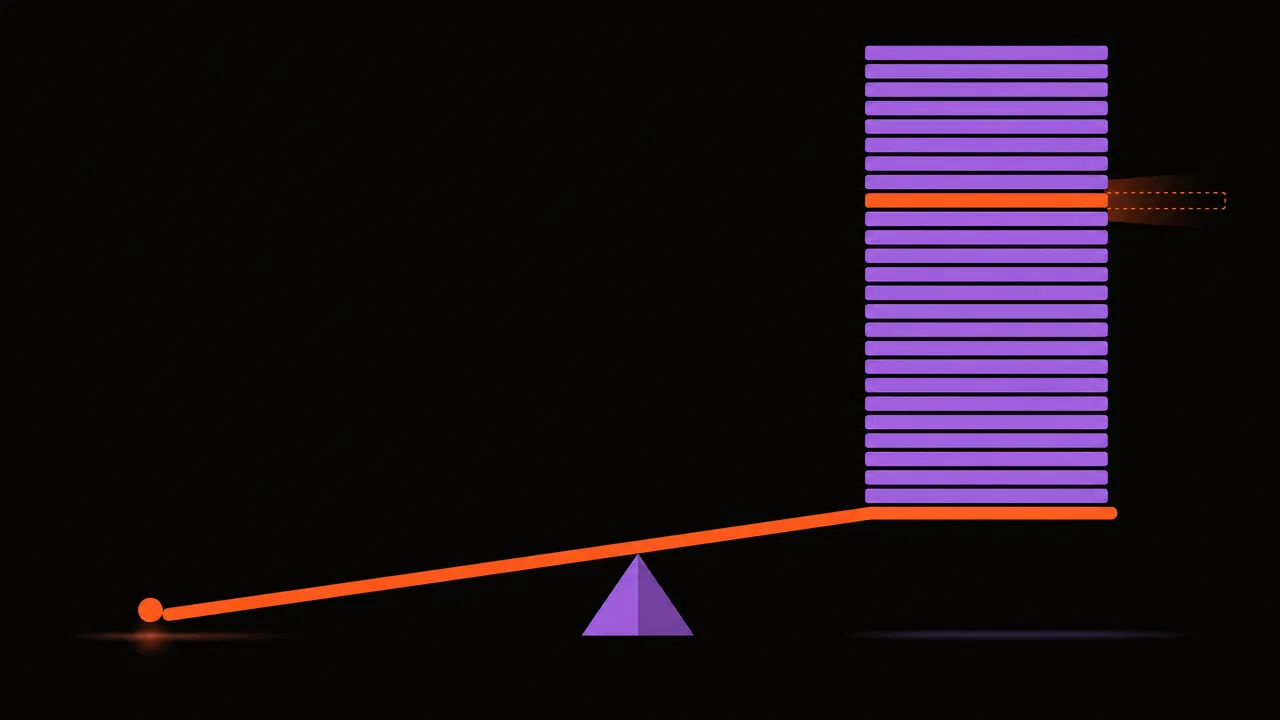

It also points you at the smallest possible payoff. You can win the latte battle every single day for a year and save a few hundred dollars. Or you can spend one uncomfortable afternoon on the phone and cut a recurring bill by the same amount, permanently, with no daily effort at all. Same money, wildly different cost to you.

The bigger lever: fix the recurring, not the occasional

The most valuable expenses to attack are the ones that repeat without asking. A single successful negotiation — a lower insurance rate, a cheaper phone plan, a subscription you cancel for good — keeps paying you back every month for as long as you keep it. That is the exact opposite of the latte, which you have to give up again tomorrow, and the day after that.

Trimming a hundred dollars off your rent, insurance, or car payment often does more for your security than skipping three hundred and sixty-five coffees, and it asks for a fraction of the discipline. The leverage is enormous precisely because the cost is recurring — you do the work once and collect the difference on autopilot.

So should you feel bad about the coffee?

No — and that is the quiet thing the myth got backwards. Small spending is not the enemy, and skipping it is not virtue either. It is just small. A coffee you genuinely enjoy is one of the cheapest reliable pleasures money buys, and cutting it will not decide your financial life in either direction.

The healthier posture is to stop moralizing about the little things and start auditing the big ones. Spend on what you actually like, without the guilt, once you know the heavy, invisible costs underneath are genuinely in line. Guilt is a bad budgeting tool; attention is a good one.

What to actually do this month

You do not need a spreadsheet or a spartan lifestyle. You need one honest look at the costs you stopped questioning years ago. A short checklist to run this month:

- List every recurring charge — rent or mortgage, insurance, phone, internet, gym, and every subscription — and add them into a single total. That one number usually dwarfs a whole year of coffee.

- Reopen your two or three largest bills as if you were a brand-new customer. Insurers, lenders, and carriers often keep their best rates for people who ask; loyalty is frequently the price you pay for never calling.

- Cancel anything you would not sign up for again today. A subscription you forgot about is not a treat — it is a charge you are no longer choosing.

- Sort a month of spending by category, not by individual purchase. Categories show where the weight really sits; single transactions just make the small stuff look guilty.

- Only after the big costs are in line, decide whether any daily habit is truly not worth it to you — and keep the ones that are.

How Moneux makes the invisible visible

The reason fixed costs escape scrutiny is that nothing ever puts them all in front of you at once. Moneux groups your transactions by category and surfaces your largest, most repetitive charges, so the bills worth an afternoon of effort stop hiding behind the coffee you already feel bad about. The latte was always the wrong number to stare at. The point was never to spend less on what you notice — it was to finally notice what you were spending.

See where the money actually goes

Moneux groups every transaction by category and surfaces your largest recurring costs, so the expenses worth renegotiating stop hiding behind the small ones you already notice.