What your bank balance actually shows

Your bank balance is a snapshot of money that has cleared into your account right now. It says nothing about what is already spoken for: the rent that debits on the 1st, the credit card minimum due Friday, or the $200 you promised yourself for an emergency fund. A balance is a fact about the past few transactions, not a forecast.

What "available money" should account for

Available money is what's left after you subtract every commitment you already know about. That includes upcoming bills before your next paycheck, minimum debt payments due soon, transfers you've committed to savings or goals, and a small safety buffer for the unexpected. Two people with the same $2,400 balance can have very different amounts of money they can actually spend today.

A worked example

Say Maya checks her banking app and sees $2,400. It feels like a fine week to book a flight. But $1,400 in rent debits in four days, a $180 card minimum is due in six, she's already committed $200 a month toward her emergency fund goal, and she keeps a $100 buffer for the unexpected. Run the subtraction — $2,400 − $1,400 − $180 − $200 − $100 — and her actual available money is $520, not $2,400. The flight might still be fine, but that's a decision made with the real number, not the one her banking app happened to show that morning.

A simple formula you can use today

Available = Balance − Upcoming payments (before next income) − Committed savings/goal transfers − Safety buffer.

- List every bill due before your next paycheck, even ones not yet charged.

- Subtract minimum payments on cards or loans due in that window.

- Subtract anything you've already committed to a goal or emergency fund.

- Keep a small buffer (even $50–100) for irregular fees or price changes.

Why this gap causes real damage

The classic failure mode: balance looks healthy on the 25th, so a purchase feels safe. Then rent debits on the 1st and a card payment clears on the 3rd, and the account is short before the next paycheck lands. None of those payments were a surprise — they just weren't subtracted from the number being looked at.

Common mistakes that quietly shrink your available number

Even people who do the subtraction get the result wrong sometimes, usually for one of these reasons:

- Forgetting irregular bills — insurance, annual subscriptions, or a yearly fee — because they don't show up most months.

- Treating gig or freelance income as already available before it actually clears, not after.

- Double-counting money in a joint account that a partner is also planning to spend.

- Counting a bonus or tax refund as available the day it's announced rather than the day it lands.

What changes when your income is irregular

Freelancers, gig workers, and anyone paid on commission have an extra wrinkle: "next paycheck" isn't a fixed date. The fix isn't to guess — it's to calculate available money against your next confirmed payment, not an estimated one, and treat any income you haven't invoiced or been told a date for as not existing yet. It's more conservative than necessary most months, but it means the number is never wrong in the direction that causes a shortfall.

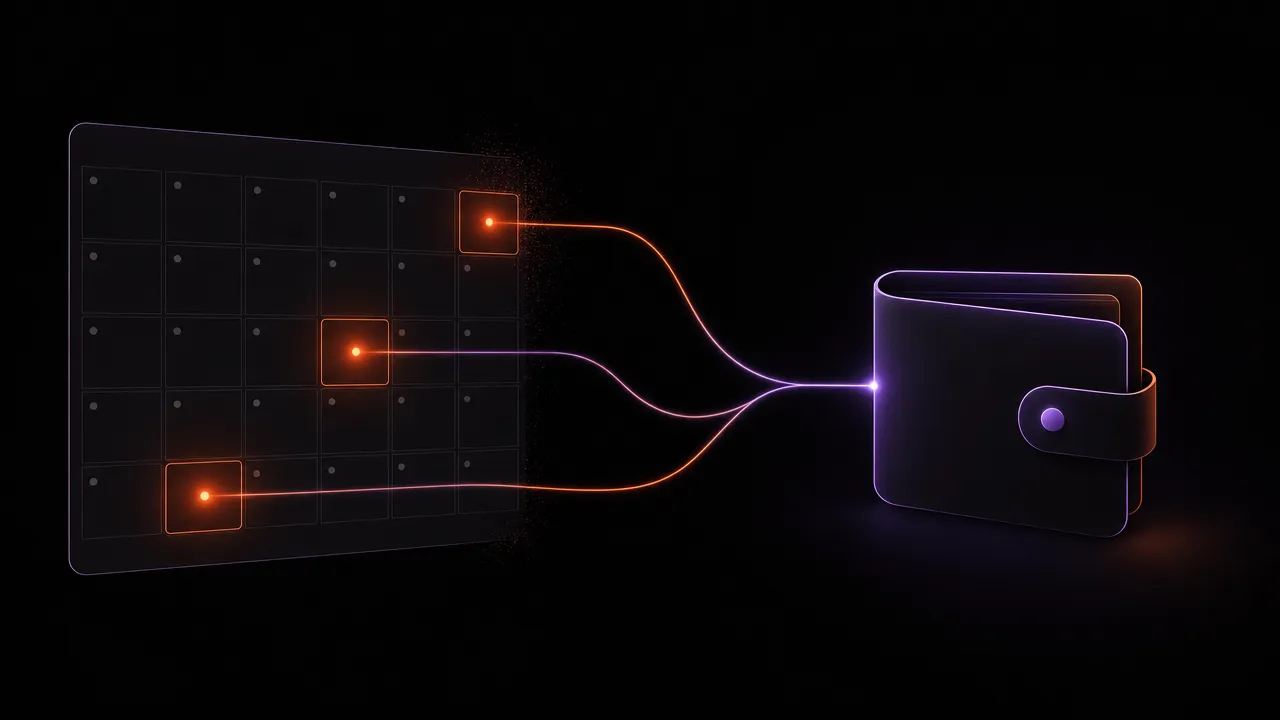

How Moneux automates this

Moneux's Available screen runs this calculation continuously: balance, upcoming payments, committed transfers, and a safety margin, combined into one number you can trust before you buy something. It also catches the irregular bills and committed transfers above, since they're tracked once and then factored in automatically every time the number updates.

See your available money automatically

Moneux calculates available money from your balance, upcoming bills, and committed savings — updated every time you log a transaction.