The money is spent before it arrives

The deposit hasn't cleared yet, and you have already spent it. Not in your bank — in your head. The bonus becomes a weekend away. The tax refund becomes the thing in your cart you keep almost buying. The inheritance becomes a vague, warm sense that things are finally going to be easier. None of it has happened, and it is already gone.

That is the strange danger of found money. A windfall arrives with no instructions and no history, so it feels lighter than the money you earned two weeks ago and guarded carefully. The number is real. The plan is not. And a lump sum without a plan has a short half-life.

A windfall is not a raise

The core mistake is quiet and almost universal: we treat a one-time amount as if it were recurring. A raise changes every future paycheck, so it can justify a slightly bigger life. A windfall lands once. If it funds a habit — a nicer subscription tier, a standing dinner reservation, a car payment — the habit outlives the money by years.

Behavioral economists call the underlying reflex mental accounting: we tag money by where it came from instead of what it can do. Earned money gets careful treatment. 'Found' money gets loose treatment. But a dollar from a bonus buys exactly what a dollar from your salary buys. The only real difference is the story you attach to it, and the loose story is the expensive one.

First, find out what you actually keep

Before you allocate a windfall, find the real number. The headline figure is rarely what lands in your account. A bonus can be taxed at withholding rates that surprise people. Proceeds from selling something, certain inheritances, and investment gains can carry their own tax and fee consequences. A 'ten thousand' windfall might be closer to seven by the time it settles.

This matters because most regret comes from planning against the big number and spending against it before the smaller, true number shows up. Wait for the amount to actually clear, confirm what is yours after taxes and fees, and only then decide what it can do. Planning against a figure you will not keep is how people end up funding a lifestyle with money that was never really there.

Give it a boring place to sit

The most underrated move with a windfall is to do almost nothing at first. Regulators and planners often suggest a deliberate cooling-off period — for a large sum, even several months — with the cash parked somewhere safe and unexciting, like a high-yield savings account. Not because saving is virtuous, but because urgency is what fraudsters and impulse both feed on.

A cooling-off period does something subtle. It separates the emotion of receiving from the decision of allocating. The excitement fades, the pressure from other people fades, and what is left is a calmer version of you making the call. Very few good money decisions get worse by waiting two weeks. Many bad ones would have been avoided by exactly that pause.

The order that quietly builds wealth

Once you know the real number and the rush has passed, a simple sequence handles most of the work. It is not glamorous, and that is the point. You are not trying to be clever; you are trying not to waste a rare chance to move your baseline up.

- Top up a cash cushion first, so the next surprise expense does not become new debt.

- Clear high-interest debt next — paying off a card is one of the best 'investments' available, because the rate you stop paying is usually higher than any return you'd reliably earn.

- Fund your named goals — split them into short, medium, and long term, and give each its own bucket so progress stays visible.

- Invest what remains for the long term, and if an employer match is on the table, route your regular income to capture it while the windfall covers your living costs.

Notice the logic: safety, then the near-guaranteed return of killing interest, then goals you can name, then growth. You can adjust the order for your situation — a punishing interest rate might jump the line ahead of savings — but the shape holds. Boring, in this order, compounds.

Pay yourself a slice, on purpose

None of this means you have to be a monk about it. A windfall you never enjoy is its own kind of failure — it teaches you that good financial behavior feels like punishment, and that lesson makes you worse with money over time. So carve off a deliberate slice, something like a tenth to a fifth, and spend it with zero guilt.

The distinction is intention. 'I set aside this amount to enjoy' is a decision. 'It kind of evaporated on nice dinners and I'm not sure where' is a leak. Same money, opposite outcomes. Celebrate on purpose, then let the rest go to work.

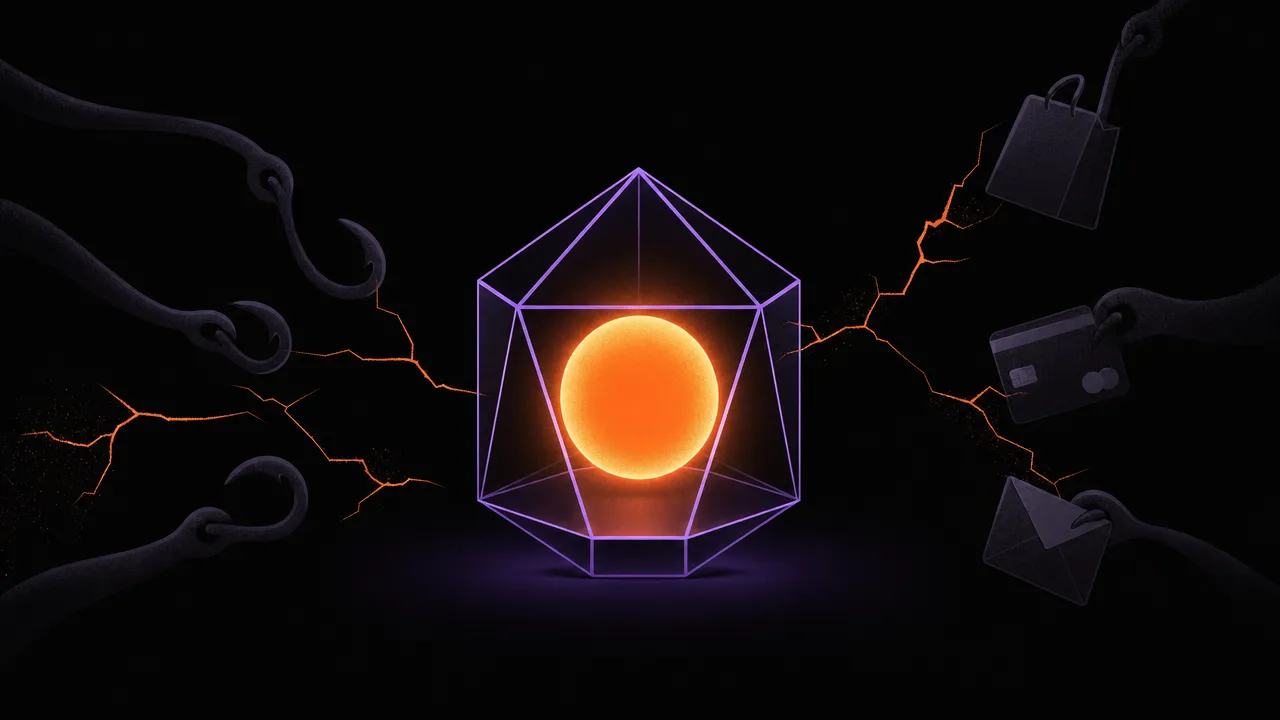

The two things that drain found money

Two forces quietly compete for a windfall, and both are easy to miss until the money is gone.

- Lifestyle creep: the upgrades that feel earned in the moment and become fixed costs forever — the bigger plan, the nicer everything, the standing expense you can no longer picture living without.

- Scammers and 'sure things': a windfall, especially a visible one, makes you a target. Pressure to act now, promises of guaranteed or outsized returns, and secret strategies are red flags, not opportunities.

The defense against both is the same cooling-off period from earlier. Creep and fraud thrive on speed and emotion. A plan you wrote while calm is remarkably good at saying no on your behalf later.

How Moneux keeps a windfall from evaporating

This is where seeing your money helps more than willpower does. Moneux shows your available money, your goals, and your debts in one place, so a windfall becomes something you assign on purpose instead of something that quietly disappears into a normal-looking month. You can watch the cushion fill, the debt shrink, and each goal move closer — which is exactly the feedback that keeps the plan intact.

A windfall is rare. That is the whole reason to slow down with it. Treat it like income and it becomes an ordinary month you can barely remember. Treat it like the one-time event it is, and it can quietly reset your baseline for years.

See where a windfall should go

Moneux shows your available money, goals, and debts in one place, so found money gets assigned on purpose instead of disappearing into an ordinary month.