Why 'irregular' expenses are a myth

Car registration, holiday gifts, annual insurance renewal, a dentist checkup — these costs feel unexpected because they don't land every month. But they all arrive on a predictable schedule. The real problem isn't unpredictability: it's that most budgets only track the things that recur every 30 days and silently exclude everything else. So a $600 car registration in March looks like a budget crisis even though it appeared on the same schedule the year before.

What a sinking fund actually is

A sinking fund is a designated savings pool for a single, known future expense. The idea is simple: estimate what the cost will be, divide by the number of months until you need it, and move that fraction into a dedicated fund every month. When the expense arrives, the money is already there. No emergency fund withdrawal needed, no credit card balance to carry afterward. The name sounds complicated, but the practice is just "save in advance for a specific thing."

Sinking fund vs. emergency fund: not the same thing

The confusion is understandable, but they solve different problems. An emergency fund is for the genuinely unexpected — a medical bill you couldn't have planned, a job loss, a repair that came out of nowhere with no warning. A sinking fund is for the known but irregular — things you can put on a calendar right now. Car registration is a sinking fund category. A hospital stay after an accident is an emergency fund category. Mixing them up means the emergency fund slowly drains to pay for things that were never really emergencies, and then it isn't there when an actual emergency hits.

Common categories to start with

There's no official list, but these categories catch most people's recurring blindspots:

- Car maintenance and registration: oil changes, tires, annual tags, smog checks, and the repairs that aren't surprises if you own a car long enough.

- Holiday and gift-giving: presents, decorations, travel to see family, the office gift exchange — a fixed date every year.

- Annual subscriptions and memberships: software licenses, gym memberships, professional dues, domain renewals paid once a year.

- Home maintenance: a reserve for the repairs every home eventually needs — plumbing, roof, appliances, HVAC.

- Medical and dental: checkups, glasses, routine procedures not fully covered by insurance, dental work scheduled in advance.

- Travel and vacations: a dedicated fund per trip so the money doesn't come from a general savings pool that has other jobs.

- Pet care: annual vet visits, vaccinations, and a small buffer for the unexpected vet bill that's less surprising than it feels.

You don't need all seven at once. Start with the two or three that caused the most financial stress in the past year and add more as the habit settles in.

How to calculate the monthly number

The math takes about two minutes. Say your car insurance renews in six months and you expect the annual premium to be around $1,200. Divide by six: you need to set aside $200 a month to have it covered. Same logic for a vacation: if a trip will cost roughly $1,800 and you want to take it in nine months, $200 a month gets you there without touching any other savings. Once you've run the numbers, you can automate the transfer on payday so the decision never has to be made again — the money moves before you have a chance to spend it elsewhere.

How many sinking funds is too many

There's no universal answer, but a practical limit comes from a different direction: if you have too many small funds scattered across too many accounts, the overhead of tracking them creates its own friction. A common approach is to start with three to five categories grouped loosely by theme — for example, a "vehicle" fund that covers maintenance, registration, and eventual replacement; a "home" fund that covers maintenance and appliances. The grouping matters less than having the money separated from everyday spending before you need it.

Some people run all their sinking funds in a single savings account and track the sub-totals mentally or in a notes app. Others prefer a separate sub-account per category. Either works as long as the money isn't sitting somewhere it can be accidentally spent on something else before the bill arrives.

Funding order: where sinking funds fit in the budget

Sinking funds live in the savings bucket of any budget, but they're not the same priority as an emergency fund or retirement contributions. A sensible sequence:

- Emergency fund first — even a small starter amount — before anything discretionary.

- Minimum debt payments come before any discretionary saving.

- High-priority sinking funds next: things with a near-term date and a fixed cost, like annual car insurance or a registration due in three months.

- Longer-term goals and retirement contributions after that.

- Discretionary sinking funds last: vacation, gifts, electronics — the ones where the date or amount is flexible.

When a specific date is closing in fast, temporarily boost that fund's contribution and reduce a lower-priority one. Once the expense is paid, redirect the freed-up amount back.

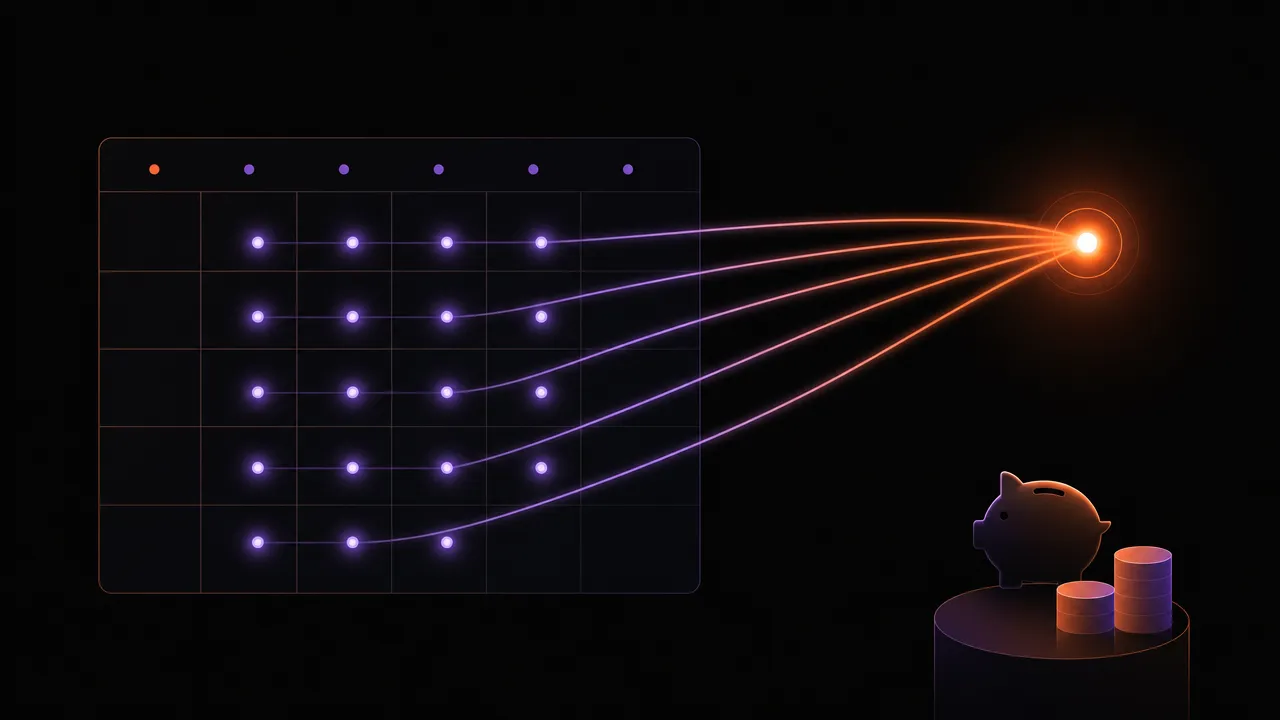

How Moneux keeps your sinking funds on track

Moneux's Goals screen lets you set a name, target amount, and deadline for each sinking fund — so instead of tracking sub-totals in a notes app, you see each fund's progress and monthly contribution requirement in one view. And because committed transfers are subtracted from your Available number automatically, the money earmarked for car registration or holiday gifts doesn't silently get spent on something else before it's needed.

Give every irregular expense its own fund

Moneux's Goals screen tracks each sinking fund separately — name, target, deadline, and how much more is needed — so you set it up once and stop thinking about it.